Episode 10: How to Actually Prepare for Baby – The MillennialFI

We made it to 2021!

Welcome to TheMillennialFI. Let’s all take a breath and savor this achievement. For many past years, I’ve started out with new goals. This time I want to do things a little different because new year resolutions are out dated and tend to work against us.

It’s not really a goal but a set place I want to reach in life.

The last few decades I’ve managed to live on a mix of sheer will, happenstance, privilege, and loss. This decade isn’t going to be any different but I’m more prepared for whatever life can throw in my path. As a millennial, the financial sector of my life has been a burning dumpster fire as some of my friends would say. So who am I to give you advice? It’s simple. I’m not advising Jack. I’m simply someone that moves through life utilizing what tips, tricks, and loopholes are available to her.

My mission for The MillenialFi is to document my family’s journey to financial independence, including the tools and methods utilized. Because anyone can be financially independent. It’s a matter of will, discipline, and math. Lot’s of math in fact. This year, we’re setting out to prove we can do this!

Let’s recap.

2020, for better or worse, was surprisingly beneficial to our financial life. Yes, I was laid off because of the virus. No, I did not let that fact hold me back. It actually helped me break from a toxic employer and industry that I’d been trying to move up or move out of for 6 years with no success.

And so with a new lease on our career and financial lives, we’re moving into the next decade with the mindset to achieve financial independence by the time my husband is 40. With it, we’re creating this website TheMillennialFI to document our path. Currently, we’re looking at roughly 11 years or 2032 that we will be Financially independent by. Will we hit the goal on time? We shall see! It will take a combination of investment smarts, discipline, and setback mitigation.

As with everything on the internet, you should take the methods and tools I’ll be mentioning over the life of this blog with a grain of salt. There’s no such thing as a one-size fits all formula and only you truly know what is best for you and your financial situation. However, I hope TheMillennialFI posts bring some clarity to an often complicated topic and inspiration for you to seek your own independence and freedom from the traditional life of “living for the weekend”.

Let’s review our starting point.

While 1 million is an inspiring number, based on a myriad of calculations, we only truly need 650k across our assets to be financially independent. Obviously more would be beneficial but is not necessary to reach FI.

I should preface that financial independence is not about getting rich quick or never working another day. It’s about being secure enough to follow your true passions and savvy enough to not deplete the funds you worked so hard to build. We’re talking about living on residuals so that our balance continues to grow even after we achieve goal.

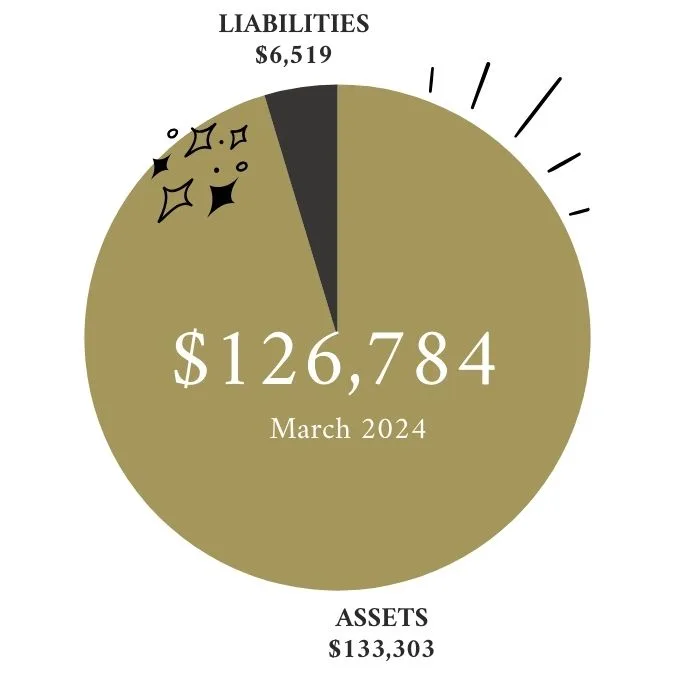

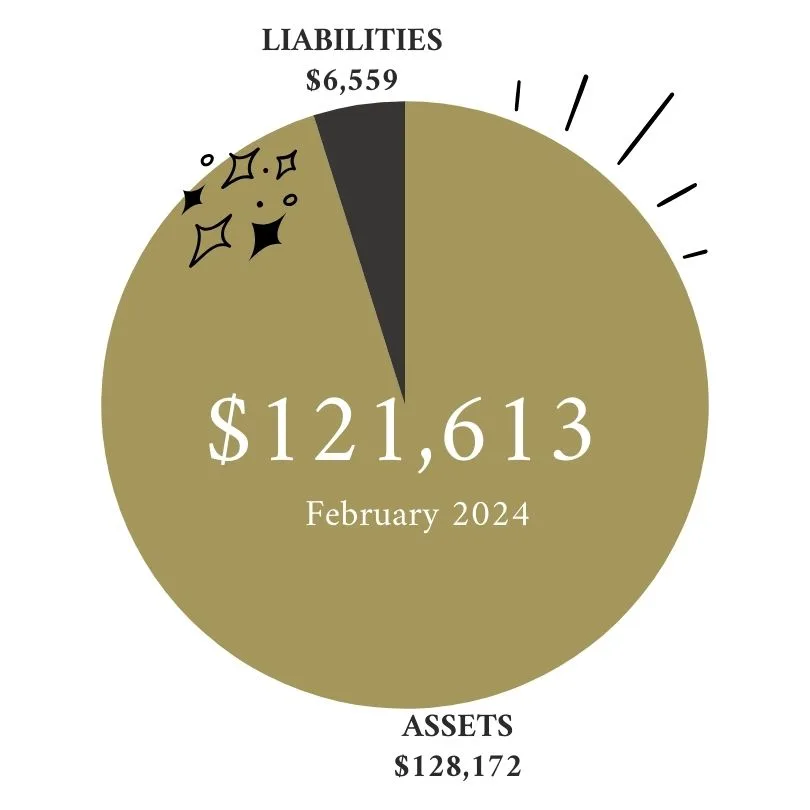

For simplicity, I’m rounding the numbers. My husband and I are entering 2021 with credit scores of around 750.

Our consumer debt looks like this:

- Student loans – $6700

- Mortgage – $157,800

- Second mortgage – $7900

Our assets are:

- 401k/retirement/investment – $10,000

- Liquid accounts – $17,000

- Real Estate – $165,000

- Car – $4500

Considering our age, our savings is not ideal but it’s better than where we were in 2019 which was basically broke and bleeding money trying to make life in Canada work. It’s crazy to think back, less than 10 years ago, we were homeless with $500 to our name, no credit history and scarce career history. It takes time and effort to come back from situations like that and it brings its own physical and psychological challenges I may cover in later posts here at TheMillennialFI. But that’s why I say if we can do this, anyone can.

#ThePlan

For this first quarter, we’re aiming to cull wasteful expenses and reach a 35% savings rate. Our biggest controllable bill is food and miscellaneous spending. Our current savings rate from the last quarter was roughly 30%. We had just moved into our new house and had a few unexpected medical setbacks to pay off.

In terms of debt, we’re looking to paydown my student loans which have the highest interest rate – around 6.725%. By paying those off first, we can then apply the monthly payments to our main mortgage loan, essentially keeping our monthly debt payments the same while paying them down faster. The second mortgage is only at 1% so is not an immediate priority, although we do allocate additional funds to pay it off faster.

Getting to 650k is going to be a journey so until then, let’s play with FIRE! Don’t forget to subscribe to TheMillennialFI blog and podcast to keep up to date on our adventures and hopefully learn something handy in the process.

Take a moment to think about what it is you really want in life. What actually makes you happy or content and what do you need to do to get there?